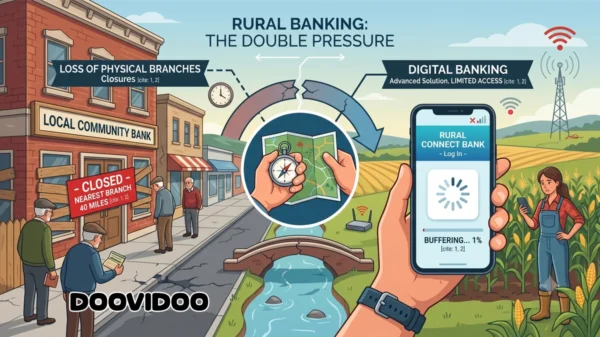

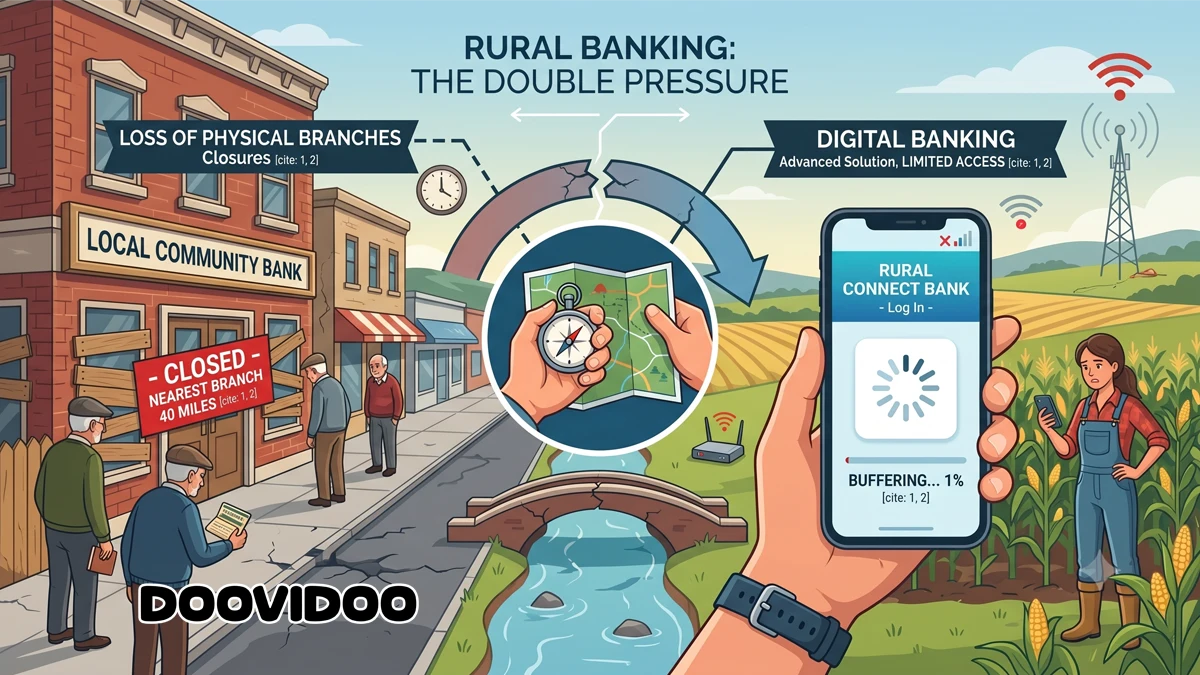

Rural banking faces a double pressure. On one side, many communities are losing physical bank branches. On the other side, digital banking is advancing as the main solution, although millions of people still lack reliable access to high speed internet.

The problem is not minor. A bank account allows people to receive payments, save money, request credit, pay bills, send money, and build financial history. When a rural community loses its local bank, it does not lose only an office. It loses a point of trust, advice, and direct access to the financial system.

Digitalization promises to solve part of the problem. An app allows users to check balances, transfer money, pay bills, and deposit checks from a phone. But that solution requires three conditions: stable connection, a proper device, and digital skills. In many rural areas, those three conditions are not guaranteed.

That is why talking about rural banking requires looking at two gaps at the same time. The banking gap and the technology gap. When both cross, financial inclusion weakens.

What Rural Banking Means

Rural banking includes the financial services available to people, families, farmers, small businesses, and organizations located outside major urban centers. It includes checking accounts, savings accounts, loans, mortgages, agricultural credit, payments, remittances, insurance, and financial advice.

In urban areas, a person usually has several nearby options. Banks, credit unions, ATMs, lending offices, apps, and fintech services. In rural areas, the map changes. Distances are longer. Public transportation is limited. Mobile signal fails in some places. Fixed internet does not always reach every home. The closure of one branch can affect an entire town.

Rural banking also has a social function. The manager of a local branch knows merchants, farmers, and families. That knowledge helps evaluate risks that do not always appear in a digital application. A small business with variable income needs more than an algorithm. It needs an institution that understands the local economic cycle.

Branch Closures and Loss of Access

The numbers show a clear reduction of bank branches in rural areas of the United States. The Federal Reserve reported that between 2012 and 2017, more than 40 percent of rural counties lost bank branches. During that period, rural counties that lost offices recorded a net reduction of 1,533 branches. Overall, rural areas ended with a net loss of 1,332 branches.

The strongest figure appears in the most affected counties. The Federal Reserve identified 44 counties that had 10 branches or fewer in 2012 and lost at least half by 2017. Of those 44 counties, 39 were rural. This shows that the impact is not distributed equally. Communities with less infrastructure lose more when a bank office closes.

The closure of a branch in a large city is inconvenient. The closure of a branch in a small town changes daily life. An older adult must travel farther. A business must close for hours to make a deposit. A farmer loses contact with a local lender. A family without a car depends on favors or extra payments.

The Federal Reserve also found that rural communities most affected by branch closures tend to have more poverty, lower incomes, and lower educational attainment than other rural counties. This worsens the problem. The areas that most need nearby access to financial services are the same areas facing the greatest loss of offices.

Banking Deserts and Real Distance

A banking desert is an area where there is no bank branch within a defined distance. Fed Communities defines that distance by community type: 2 miles for urban areas, 5 miles for suburban areas, and 10 miles for rural areas.

The rural standard recognizes a basic reality. Distances are longer. But even with that margin, many residents remain far from the nearest bank. In an analysis from the Federal Reserve Bank of Philadelphia, rural banking deserts in 2023 had an average distance of about 19.5 miles to the nearest branch. In majority Native communities, the average distance reached 30.6 miles.

That distance has a cost. Cost of gas. Cost of time. Cost of missing work hours. Cost of depending on someone else. For a family with limited income, every financial trip matters.

Distance also affects safety. Some older adults withdraw larger amounts of cash because they do not want to travel several times. That increases the risk of loss or theft. Others avoid opening new accounts because the bank is too far away. Others turn to alternative services with higher fees.

Digital Banking: An Incomplete Solution

Digital banking reduces part of the friction. It allows simple transactions without travel. It also helps banks that no longer see profit in keeping an office with low foot traffic.

But digital banking does not replace everything. It does not solve every complex dispute. It does not always make a small business loan easier. It does not help someone without stable internet. It does not work the same for someone who does not know how to manage apps. It does not replace trust built inside a community.

The FDIC reported that in 2023 almost half of banked households in the United States, 48.3 percent, used mobile banking as their main method to access accounts. That figure confirms the digital shift. But it also shows the risk of leaving behind people who are not connected.

Digital progress benefits people who already have a device, a connection, and financial education. A person with good internet checks an account in seconds. Another person with poor signal waits, fails, calls the bank, or travels. The same service does not create the same access.

The Technology Gap in Rural Areas

Rural banking depends more and more on internet access. But broadband access remains incomplete. The Federal Communications Commission updated its fixed broadband benchmark in 2024 to 100 megabits per second download and 20 megabits per second upload. Under that standard, the FCC stated that 24 million people in the United States lack access to fixed broadband connectivity.

The U.S. Department of Agriculture also reported that in June 2023 more than 14 percent of rural households lacked broadband access, compared with 3 percent of households in metropolitan areas. In tribal areas, the figure was close to 12 percent.

These data matter for financial inclusion. Without fast internet, a banking app becomes fragile. A video call with an adviser fails. A mobile check deposit does not load. A loan application remains incomplete. A farmer cannot review payments or financing on time.

The technology gap also affects small businesses. A rural store needs to accept card payments, pay suppliers, check inventory, request credit, and file taxes. If the connection fails, operations become slower and more expensive.

Basic Financial Services: City Versus Rural Area

The difference between urban access and rural access appears in simple services.

Opening an account in a city often requires a short trip or a quick digital application. In a rural area, the applicant may need transportation, time off, and physical documents. If the nearest bank is 20 miles away, the account has a hidden cost from the first day.

Depositing cash also changes. A restaurant, gas station, or small store needs to make frequent deposits. Without a nearby branch, the owner travels, pays fees, or keeps more cash on hand. That increases risk and reduces efficiency.

Requesting credit becomes harder. Local banks understand the local economy better. When they close or consolidate, decisions move farther away. A remote lender evaluates with standardized data. That evaluation may ignore agricultural seasonality, local relationships, or nontraditional income.

Solving problems also costs more. An unknown charge, blocked card, failed transfer, or suspected fraud requires fast attention. In a city, the customer can visit an office. In a rural area, the customer must call, wait, or travel.

Older Adults and Small Businesses

Older adults feel the change more strongly. Many depend on fixed incomes, feel less comfortable with apps, and prefer in person service. When a branch closes, they must learn technology, depend on relatives, or pay for transportation.

Small businesses also lose. The Federal Reserve gathered testimony from rural communities where business owners had to close for hours to travel to the bank. Some reported higher costs for card payments, less cash availability, and loss of local commercial activity.

The bank also acted as a civic point. It sponsored events, participated in chambers of commerce, advised families, and supported local organizations. When it disappears, the community loses more than counters and desks.

Financial Inclusion and Alternative Services

When rural banking fails, alternative services grow. Check cashing stores, money orders, payday loans, prepaid cards, and nonbank apps fill part of the gap. Some services help in specific cases. Others raise the cost of financial life.

The FDIC reported that in 2023, 4.2 percent of U.S. households did not have a bank account. That equals 5.6 million households. It also reported that 14.2 percent of households were underbanked, meaning they had a bank account but still relied on nonbank products to meet financial needs.

The problem is not having a payment app. The problem appears when a family depends on more expensive alternatives because it does not have simple access to a safe account, fair credit, or reliable service.

What Rural Banking Needs

The solution should not depend on one single path. Reopening every closed branch will not always be viable. Moving everything to an app also does not solve the problem.

Rural banking needs mixed models. Shared branches. Credit unions. Community banks. Mobile units. Secure ATMs. Agreements with post offices or local businesses. Financial education. Human phone support. Light digital platforms that work with weak connections.

It also needs broadband. Without internet, digital banking remains limited. Investment in connectivity must be seen as financial policy, not only technology policy. Every connected rural household gains access to banking, education, health care, commerce, and public services.

Banks must design products for rural reality. Flexible hours. Simple processes. Accessible verification. Support for older adults. Credit for businesses with seasonal income. Bilingual service where needed. Protection against digital fraud.

Rural Banking and the Financial Future

Rural banking defines who participates in the modern economy. A community without a nearby bank and without fast internet remains at a disadvantage. It pays more for basic services. It travels more. It waits more. It accesses less credit. It builds less financial history.

Technology helps, but it is not enough. Financial inclusion requires presence, trust, and connectivity. If a person has an account but cannot manage it with ease, access is incomplete. If they have an app but lack broadband, the service fails. If they have a bank 30 miles away, the real cost rises.

Rural banking needs a strategy that brings together physical infrastructure, human service, and digital access. The financial future of rural communities does not depend only on closing the banking gap. It also depends on closing the technology gap.

Sources used: The Federal Reserve reported that between 2012 and 2017 more than 40 percent of rural counties lost bank branches, with 1,533 net closures in rural counties that lost offices and 39 of the 44 most affected counties classified as rural.

Fed Communities defines banking deserts by distance to a branch and states that digital banking requires a modern device, internet access, and skills to manage websites or apps.

The Federal Reserve Bank of Philadelphia reported that rural banking deserts in 2023 had an average distance of 19.5 miles to the nearest branch, and 30.6 miles in majority American Indian and Alaska Native banking deserts.

The FDIC reported that in 2023, 4.2 percent of U.S. households were unbanked, 14.2 percent were underbanked, and 48.3 percent of banked households used mobile banking as their main access method.

The FCC stated in 2024 that 24 million people in the United States lacked access to fixed broadband, and the USDA reported that in June 2023 more than 14 percent of rural households lacked broadband, compared with 3 percent in metropolitan areas.